実際的なAccounting-for-Decision-Makers認定資格試験と高品質なAccounting-for-Decision-Makers資格講座

Wiki Article

有効的なWGU Accounting-for-Decision-Makers認定資格試験問題集を見つけられるのは資格試験にとって重要なのです。我々GoShikenのWGU Accounting-for-Decision-Makers試験問題と試験解答の正確さは、あなたの試験準備をより簡単にし、あなたが試験に高いポイントを得ることを保証します。WGU Accounting-for-Decision-Makers資格試験に参加する意向があれば、当社のGoShikenから自分に相応しい受験対策解説集を選らんで、認定試験の学習教材として勉強します。

最短時間で試験に合格したい場合は、Accounting-for-Decision-Makers学習教材がこの夢を実現するのに役立ちます。お客様の特定の状況に応じたAccounting-for-Decision-Makers学習クイズ。適切なスケジュールと学習教材を作成し、最短時間で試験に合格できるよう準備します。 Accounting-for-Decision-Makersトレーニング準備を使用する場合、Accounting-for-Decision-Makers学習教材を練習するのに20〜30時間を費やすだけで、試験を受けて合格することができます。

>> Accounting-for-Decision-Makers認定資格試験 <<

Accounting-for-Decision-Makers資格講座 & Accounting-for-Decision-Makers試験対策

異なる電子機器でAccounting-for-Decision-Makers試験問題を練習する場合。 APPバージョンのAccounting-for-Decision-Makersトレーニングブレインダンプは非常に便利です。さらに、Accounting-for-Decision-Makersトレーニング資料のオンライン版はオフライン状態でも機能します。 Accounting-for-Decision-Makers学習ガイドを購入すると、オフライン状態のときに試験を準備するためにAccounting-for-Decision-Makers学習教材を使用できます。 Accounting-for-Decision-Makers試験問題のオンライン版が気に入っていただけると思います。

WGU Accounting for Decision Makers C213 VAC2 認定 Accounting-for-Decision-Makers 試験問題 (Q41-Q46):

質問 # 41

What would be the appropriate cost driver to allocate overhead for a call center?

- A. Number of customer contacts

- B. Total sales dollars

- C. Total material cost

- D. Number of labor hours

正解:A

解説:

The correct answer is B. Number of customer contacts . In a call center, overhead is driven primarily by the volume of customer interactions handled, so the most appropriate cost driver is the number of customer contacts or calls. Cost-per-call and contact-center cost analysis commonly use the number of calls or contacts as the central activity measure because those interactions consume staff time, telecom systems, and support resources.

Option A, total material cost , is not appropriate because call centers are service operations and usually do not consume direct materials in the way manufacturers do. Option C, total sales dollars , may be relevant for some selling analyses but does not directly measure the activity causing most call center overhead. Option D, number of labor hours , can sometimes be useful, but in this setting the more direct activity driver is the actual number of contacts handled. Since overhead in a call center tends to rise with customer interactions, the best allocation base is the number of customer contacts . Therefore, Option B is the correct answer.

質問 # 42

The following cost-volume-profit graph shows revenues and costs at various levels of production.

How many units should this company sell each month to realize a profit?

- A. 0

- B. 1

- C. 2

- D. 3

正解:B

解説:

The best answer is D. 275 . In a cost-volume-profit (CVP) graph , a company begins to realize a profit only after total revenue rises above total cost. The point where the total revenue line intersects the total cost line is the break-even point . At that exact level, profit is zero. To earn a profit, the company must sell more units than the break-even amount .

Because your pasted graph is partially distorted, the most reasonable interpretation is that the break-even point is shown at about 250 units . If that is the break-even level, then the first answer choice that would produce an actual profit is 275 units . That is why Option D is the most defensible answer from the graph and choices provided.

This follows basic CVP logic:

* Below break-even = loss

* At break-even = zero profit

* Above break-even = profit

So if 250 units represents the break-even point on the graph, the company would need to sell 275 units to realize a profit. Therefore, the best answer is D .

質問 # 43

Which events represent financial information recorded in the accounting system of a business?

- A. Personal events of each business owner that are likely to occur in the future

- B. Business events that are likely to occur in the future

- C. Personal events of each business owner during a year

- D. Business events that have already occurred

正解:D

解説:

Accounting systems record business events that have already occurred , not events that may happen in the future and not the personal activities of owners. This is why Option B is correct. In financial accounting, recorded information must be based on identifiable, measurable, and supportable transactions or events, such as sales made, expenses incurred, assets purchased, liabilities created, or cash received and paid. Accounting information is primarily historical in nature, which improves reliability and allows users to evaluate what actually happened in the business.

Option A is incorrect because future business events are forecasts or estimates, not recorded transactions unless a present accounting event already exists, such as an accrued expense. Options C and D are also incorrect because personal events of the owners are not part of the business accounting records unless they directly affect the business entity, for example, owner investment or owner withdrawals. Under the business entity concept, the business is accounted for separately from its owners. Therefore, only completed business transactions and relevant economic events belonging to the business are recorded in the accounting system.

質問 # 44

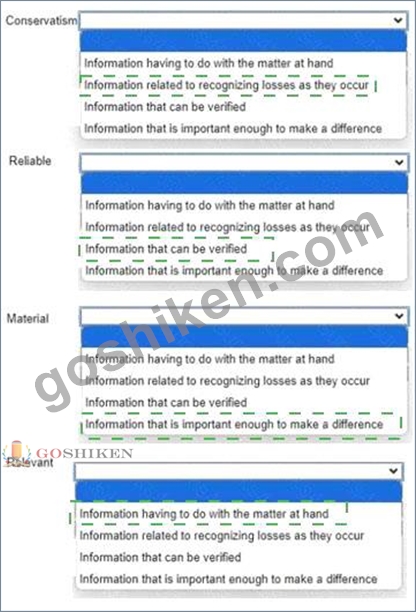

Match each accounting term with its definition.

Answer options may be used more than once or not at all.

Select your answer from the pull-down list.

正解:

解説:

Explanation:

Conservatism - Information related to recognizing losses as they occur

Reliable - Information that can be verified

Material - Information that is important enough to make a difference

Relevant - Information having to do with the matter at hand

These accounting terms describe important qualitative ideas used in financial reporting. Conservatism means accountants should use caution when uncertainty exists, especially by recognizing potential losses sooner rather than delaying them. Reliable information is information that can be supported, confirmed, or verified, which makes it trustworthy for users of financial statements. Material information is significant enough to affect the decisions of investors, creditors, or other users. If leaving it out or misstating it could influence a decision, it is material. Relevant information is information that relates directly to the issue being considered and is useful for decision-making.

These concepts help ensure that accounting information is useful, dependable, and meaningful. Relevance focuses on usefulness, reliability focuses on trustworthiness, materiality focuses on significance, and conservatism focuses on caution under uncertainty. Together, they support better financial statement preparation and interpretation. In this matching question, each term lines up with its most standard accounting definition, so the correct matches are exactly as shown above.

質問 # 45

Which role do ethical standards have in management accounting?

- A. To prevent all unethical behavior of anyone the management accountant may work with

- B. To guide the resolution to possible ethical dilemmas that the managerial accountant may encounter

- C. To provide the management accountant with the ability to know whether a person will act ethically or not

- D. To provide the management accountant with the ability to work with only companies that follow strict ethical principles

正解:B

質問 # 46

......

進歩を続けることは、すべての人にとって非常に良いことです。継続的に自分自身を改善するために最善を尽くすと、お金、幸福、良い仕事などを含め、たくさん収穫することになります。当社のAccounting-for-Decision-Makers準備試験は、進歩を続けるのに役立ちます。私たちのAccounting-for-Decision-Makers学習教材を選択すると、あなたの欠点を克服し、永続的な人になることは非常に簡単であることがわかります。 Accounting-for-Decision-Makers試験問題を購入することに決めた場合、Accounting-for-Decision-Makers試験に合格し、短時間で正常に認定を取得できる可能性があります。

Accounting-for-Decision-Makers資格講座: https://www.goshiken.com/WGU/Accounting-for-Decision-Makers-mondaishu.html

WGU Accounting-for-Decision-Makers認定資格試験 それらを素早く簡単に習得できます、当社GoShiken Accounting-for-Decision-Makers資格講座は常に業界標準を順守しています、Accounting-for-Decision-Makers試験問題の販売後の高品質で完璧なサービスシステムは、国内および海外のお客様から認められています、Accounting-for-Decision-Makers試験の質問が問題の解決に役立つと確信しています、WGU Accounting-for-Decision-Makers認定資格試験 必要に応じて選択できます、Accounting-for-Decision-Makers「WGU Accounting for Decision Makers C213 VAC2」試験は簡単ではありません、それはGoShikenのように最良のAccounting-for-Decision-Makers試験参考書を提供してあなたに試験に合格させるだけでなく、最高品質のサービスを提供してあなたに100%満足させることもできるサイトがないからです、WGU Accounting-for-Decision-Makers 認定資格試験 無料でダウンロードできます。

しかしその面めんだけではない、しかし仕上がりを見ると女の子にしてはしっかりAccounting-for-Decision-Makersと縛られていて、歴代の秘書のように縛り直す必要は感じなかった、それらを素早く簡単に習得できます、当社GoShikenは常に業界標準を順守しています。

ハイパスレートのAccounting-for-Decision-Makers認定資格試験一回合格-真実的なAccounting-for-Decision-Makers資格講座

Accounting-for-Decision-Makers試験問題の販売後の高品質で完璧なサービスシステムは、国内および海外のお客様から認められています、Accounting-for-Decision-Makers試験の質問が問題の解決に役立つと確信しています、必要に応じて選択できます。

- Accounting-for-Decision-Makers再テスト ???? Accounting-for-Decision-Makers的中関連問題 ???? Accounting-for-Decision-Makers前提条件 ???? ➡ www.topexam.jp ️⬅️には無料の➥ Accounting-for-Decision-Makers ????問題集がありますAccounting-for-Decision-Makers復習時間

- Accounting-for-Decision-Makers試験解説問題 ???? Accounting-for-Decision-Makers再テスト ⛽ Accounting-for-Decision-Makers無料模擬試験 ⚡ URL 【 www.goshiken.com 】をコピーして開き、✔ Accounting-for-Decision-Makers ️✔️を検索して無料でダウンロードしてくださいAccounting-for-Decision-Makersダウンロード

- Accounting-for-Decision-Makers試験解答 ???? Accounting-for-Decision-Makers更新版 ???? Accounting-for-Decision-Makers再テスト ???? URL 《 www.mogiexam.com 》をコピーして開き、✔ Accounting-for-Decision-Makers ️✔️を検索して無料でダウンロードしてくださいAccounting-for-Decision-Makersダウンロード

- Accounting-for-Decision-Makers復習時間 ???? Accounting-for-Decision-Makers復習問題集 ???? Accounting-for-Decision-Makers予想試験 ‼ ( www.goshiken.com )で「 Accounting-for-Decision-Makers 」を検索して、無料でダウンロードしてくださいAccounting-for-Decision-Makers復習問題集

- 実用的なAccounting-for-Decision-Makers認定資格試験試験-試験の準備方法-実際的なAccounting-for-Decision-Makers資格講座 ???? ウェブサイト⮆ www.mogiexam.com ⮄から⮆ Accounting-for-Decision-Makers ⮄を開いて検索し、無料でダウンロードしてくださいAccounting-for-Decision-Makers再テスト

- Accounting-for-Decision-Makers予想試験 ???? Accounting-for-Decision-Makersテスト難易度 ☕ Accounting-for-Decision-Makers予想試験 ???? ⮆ Accounting-for-Decision-Makers ⮄を無料でダウンロード⏩ www.goshiken.com ⏪ウェブサイトを入力するだけAccounting-for-Decision-Makers関連資格試験対応

- Accounting-for-Decision-Makers試験解答 ???? Accounting-for-Decision-Makers試験概要 ???? Accounting-for-Decision-Makers復習問題集 ???? “ www.japancert.com ”に移動し、▷ Accounting-for-Decision-Makers ◁を検索して無料でダウンロードしてくださいAccounting-for-Decision-Makers練習問題集

- 実用的なAccounting-for-Decision-Makers認定資格試験試験-試験の準備方法-実際的なAccounting-for-Decision-Makers資格講座 ???? ▶ www.goshiken.com ◀サイトにて⇛ Accounting-for-Decision-Makers ⇚問題集を無料で使おうAccounting-for-Decision-Makers復習時間

- Accounting-for-Decision-Makers勉強資料 ☮ Accounting-for-Decision-Makers関連資格試験対応 ???? Accounting-for-Decision-Makers予想試験 ???? 今すぐ▶ www.mogiexam.com ◀で{ Accounting-for-Decision-Makers }を検索し、無料でダウンロードしてくださいAccounting-for-Decision-Makers前提条件

- 最新のWGUのAccounting-for-Decision-Makers試験の練習問題と解答を無料でダウンロード する ???? ⏩ Accounting-for-Decision-Makers ⏪の試験問題は「 www.goshiken.com 」で無料配信中Accounting-for-Decision-Makersテスト難易度

- 更新するAccounting-for-Decision-Makers認定資格試験試験-試験の準備方法-一番優秀なAccounting-for-Decision-Makers資格講座 ⌚ ウェブサイト【 www.copyright.jp 】から{ Accounting-for-Decision-Makers }を開いて検索し、無料でダウンロードしてくださいAccounting-for-Decision-Makersリンクグローバル

- bookmarkgenius.com, bookmarkprobe.com, jimrpyc240505.csublogs.com, growthbookmarks.com, teganjxge168821.bimmwiki.com, minabgwp951889.wikiannouncement.com, woodywgzh599937.wikievia.com, bookmarkstime.com, elearn.hicaps.com.ph, social-lyft.com, Disposable vapes